The Bank of Canada has raised interest rates again, making it more difficult for people to get a mortgage at an affordable rate. The key overnight lending rate has been raised from 0.5% to 0.75%.

With that in mind it makes sense to me that people might want to consider buying a house in a region of Toronto which is often overlooked.

Leaside is a small but quiet neighbourhood right in the middle of Toronto. Most of the homes in Leaside are traditional detached two-storey designs dating from the 1930s and 1940s, all-brick constructed, with distinctive intermixing of cut stone around entryways and front bay windows. Homes in Leaside often have exterior details such as leaded glass windows, arched / peaked entrances and broad wooden door casings. Its a level of artistry that hasn't been seen in decades and for someone like myself who enjoys older architecture, a pleasure. Inside you will typically see traditional wooden mouldings, baseboards, and floors... the type of things you'd see when visiting your grandparents.

Or in my case, my parents' farm... or the 1920s apartment building I currently live in.

I look at the architecture of some of the homes in Leaside and I just drool. They're "perfect", almost idealized, like a

Carl Schaefer painting.

Not all the homes in Leaside are what I'd call affordable. Some of the

really nice homes are $900,000 or more. Depending on where you look however there are more economical alternatives. South Leaside has a variety of semis and bungalows with price ranges hovering around $500,000.

The reason for this is because Leaside is a good place for anyone in the upper middle-class wage bracket. So that means people like myself probably couldn't afford to live there... but I can still dream right?

Sure, its not the multi-million dollar homes of Rosedale... and its not one of the soon-to-be-a-slum condos by the waterfront either. Its just a nice quiet neighbourhood with the following perks:

#1. Conveniently close to both Yonge Street and the Don Valley Parkway. Commute time to downtown is 15-30 minutes.

#2. Cycling distance from downtown. In fact there's plenty of bicycle lanes and trails in the surrounding region. (As a

bicycle mechanic, I appreciate these things.)

#3. Abundant local parkland. Serena Gundy Park, David A. Balfour Park, Moore Park Ravine, Flemingdon Park, Sunnybrook Park, Blythwood Ravine, Sherwood Park.

#4. Lots of local schools for children and teens. Maurice Cody School, Blythwood School, Bessborough Drive School, Rolph Road School, Leaside High School, Northern Secondary School, Marshall McLuhan Secondary, North Toronto CI, Don Mills CI.

#5. Oh and its only a short bicycle ride to the Ontario Science Centre, a huge chunk of parkland, fishing in the Don River and the archery range just south of the OSC (as someone who enjoys the sport of archery I can appreciate that).

The area is named after the Lea family from Lancashire, England who arrived in Canada in 1819. John and Mary Lea later built the first brick house in York township in 1829. In 1841 their son William later bought additional land and built an octagonal home which he dubbed "Leaside". The house is no longer there, but its location was where the Leaside Memorial Gardens is now.

I did manage to find a painting of the octagonal home however, shown here.

A lot has changed since Leaside was once prime farmland. Now there's three subway stations nearby, Eglinton, Davisville and Bayview, a plethora of restaurants, boutiques and a combination of small "family businesses" and larger retail stores.

The history of the area includes:

The Leaside Junction Station, one of the busiest train stations and train yards in Toronto from 1894 to 1969.

The Leaside Viaduct, a bridge built in 1927 across the Don Valley.

Residential construction in Leaside didn't begin until the 1930s. In 1967 Leaside became part of East York and eventualled was amalgamated with Toronto in 1997. The area is popular with families, since it has such quiet streets, very little crime and a large number of schools / parkland. Many parents consider it to be one of the ideal locations in Toronto to raise kids.

In the 1990s a number of "exclusive" condos and townhouses were built in the region, attracting more families to the area. Many of Leaside's local shops are geared towards children and mothers, although the area also boasts antique shops, specialty stores and pubs. There's also libraries, community centres, indoor ice arena and an indoor swimming pool, curling rink and an auditorium. The local Sunnybrook Park even has horseback riding stables.

Seriously, freaking horse stables! Who wouldn't want to live in Leaside???

Well, maybe if you were allergic to horses or you have Hippophobia (the fear of horses)... but otherwise, com'on! Leaside is like a dream neighbourhood most people can only fantasize about living in. Of course, if you have a good job and can afford to live there that is another matter entirely.

Learn more about Leaside here:

Leaside : Prime Toronto NeighbourhoodsSearch Leaside HomesA Brief History of Leaside

Heck, there might be a condo across the street that looks EXACTLY the same as your condo, but it may be a completely different community when it comes to the way it is governed and its rules.

Heck, there might be a condo across the street that looks EXACTLY the same as your condo, but it may be a completely different community when it comes to the way it is governed and its rules. Most people on the condo board of directors lack any kind of business, legal or people skills needed to manage their building, let alone dog grooming business. They are on the board because they ran for the position and got voted in on popularity. Nothing to do with skill at all. However the are responsible for a budget that could be in the millions and must also deal with sometimes complex disputes between owners and the condo corporation. This requires a working understanding of the Provincial Condominium legislation that governs their condo. Even simple decisions such as when to turn on the air conditioning requires basic understanding of how it works and how the AC will affect unit owners in different ways, like whether they are on the south or north side of the building.

Most people on the condo board of directors lack any kind of business, legal or people skills needed to manage their building, let alone dog grooming business. They are on the board because they ran for the position and got voted in on popularity. Nothing to do with skill at all. However the are responsible for a budget that could be in the millions and must also deal with sometimes complex disputes between owners and the condo corporation. This requires a working understanding of the Provincial Condominium legislation that governs their condo. Even simple decisions such as when to turn on the air conditioning requires basic understanding of how it works and how the AC will affect unit owners in different ways, like whether they are on the south or north side of the building. If any alterations to your condo were made you should check to make sure that they got the necessary approval via the condo board. Otherwise you might have to get it approved yourself, even though its after the fact, and this can be costly. You may end up paying for further inspections and certifications by plumbers, architects or engineers, things that should have been paid for by the previous owner.

If any alterations to your condo were made you should check to make sure that they got the necessary approval via the condo board. Otherwise you might have to get it approved yourself, even though its after the fact, and this can be costly. You may end up paying for further inspections and certifications by plumbers, architects or engineers, things that should have been paid for by the previous owner. 7. Status Certificate

7. Status Certificate See Also:

See Also: TREB reports 6,681 sales during October 2010, down from the 8,476 sales in October 2009.

TREB reports 6,681 sales during October 2010, down from the 8,476 sales in October 2009.

Today I posted an article on Product Reviews Canada about Looking for Homes in Georgetown. I probably should have posted it on HERE, but whatever, I am not writing it over again. So please go have a look at the article, especially if you're also considering buying a home in Georgetown (near Brampton) and then commuting to Toronto.

Today I posted an article on Product Reviews Canada about Looking for Homes in Georgetown. I probably should have posted it on HERE, but whatever, I am not writing it over again. So please go have a look at the article, especially if you're also considering buying a home in Georgetown (near Brampton) and then commuting to Toronto.

Looking to get more bang for your buck? Imagine living in a city where the local economy has collapsed and housing prices have dropped so much its ridiculous.

Looking to get more bang for your buck? Imagine living in a city where the local economy has collapsed and housing prices have dropped so much its ridiculous. Relocation for work isn’t the biggest factor in most people’s decision to move however. A study by TD Canada Trust released Wednesday says retirement (30%) is the number one choice for people to sell their home and move.

Relocation for work isn’t the biggest factor in most people’s decision to move however. A study by TD Canada Trust released Wednesday says retirement (30%) is the number one choice for people to sell their home and move.  Rosedale was once considered a suburb 100 years ago, but is now really more uptown or midtown Toronto as the city has spread and is now a megacity metropolis. It is now the 2nd wealthiest neighbourhood in Toronto (Forest Hill, where Conrad Black lives when he is not in prison is #1).

Rosedale was once considered a suburb 100 years ago, but is now really more uptown or midtown Toronto as the city has spread and is now a megacity metropolis. It is now the 2nd wealthiest neighbourhood in Toronto (Forest Hill, where Conrad Black lives when he is not in prison is #1). Historically South Rosedale was first settled by Sheriff William Jarvis (whom Jarvis Street is named after) and his wife, Mary, in 1820. Mary Jarvis' walks and horseback rides blazed the trails which would later become Rosedale's streets and forested paths that are still used today. It was Mary who gave Rosedale its name, after the wild roses that used to grow there. (Many Rosedale residents still have roses, but they're usually of the tamer variety.)

Historically South Rosedale was first settled by Sheriff William Jarvis (whom Jarvis Street is named after) and his wife, Mary, in 1820. Mary Jarvis' walks and horseback rides blazed the trails which would later become Rosedale's streets and forested paths that are still used today. It was Mary who gave Rosedale its name, after the wild roses that used to grow there. (Many Rosedale residents still have roses, but they're usually of the tamer variety.)

Technically there is three ravines that run through Rosedale. Building on the edge of a ravine is risky so its served to create natural parkland all around Rosedale, creating physical boundaries to the neighbourhood. These ravines and the wonderful old buildings / architecture is why I think its such a nice neighbourhood to cycle in and live in.

Technically there is three ravines that run through Rosedale. Building on the edge of a ravine is risky so its served to create natural parkland all around Rosedale, creating physical boundaries to the neighbourhood. These ravines and the wonderful old buildings / architecture is why I think its such a nice neighbourhood to cycle in and live in. Rosedale Park hosts a Mayfair annual party usually on the first Saturday in May, which includes rides, games, flea market and carnival-like activities. The event is run and funded by Mooredale House.

Rosedale Park hosts a Mayfair annual party usually on the first Saturday in May, which includes rides, games, flea market and carnival-like activities. The event is run and funded by Mooredale House.

The OECD notes that subprime mortgages make up 5% of mortgages in Canada. In 2007 before the recession hit the % of subprime mortgages in the USA was 33%.

The OECD notes that subprime mortgages make up 5% of mortgages in Canada. In 2007 before the recession hit the % of subprime mortgages in the USA was 33%. “They have basically encouraged people to buy houses based on cheap mortgages,” says 84-year-old Jarislowsky. “That has created the opposite effect of what was desirable.”

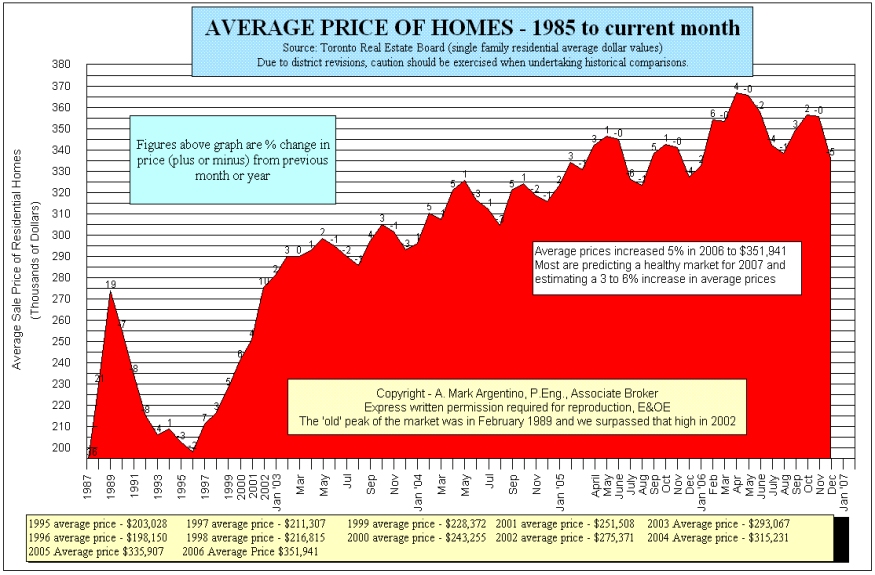

“They have basically encouraged people to buy houses based on cheap mortgages,” says 84-year-old Jarislowsky. “That has created the opposite effect of what was desirable.” The average price is still up 6% compared to last year, despite the lack of bidding wars. Realtors were hoping for a 10% increase but that didn't happen since the Toronto real estate market is shifting to a buyers market. On average prices this year are still up 8%.

The average price is still up 6% compared to last year, despite the lack of bidding wars. Realtors were hoping for a 10% increase but that didn't happen since the Toronto real estate market is shifting to a buyers market. On average prices this year are still up 8%. It was the scandal everyone was talking about in 2009, the collapse of plans by the Bazis to build a huge skyscraper condo/hotel on the site of One Bloor East. Bazis International is an architectural company from Kazakhstan with strong ties to Toronto in Canada. The company normally builds residential communities, office towers, government buildings, hotels, apartments, theatres, shopping malls, and industrial complexes.

It was the scandal everyone was talking about in 2009, the collapse of plans by the Bazis to build a huge skyscraper condo/hotel on the site of One Bloor East. Bazis International is an architectural company from Kazakhstan with strong ties to Toronto in Canada. The company normally builds residential communities, office towers, government buildings, hotels, apartments, theatres, shopping malls, and industrial complexes. The finished building was to have 189 hotel rooms and 612 condominium units. The glass and metal structure would have used the latest environmentally friendly and efficient technology making it one of the greenest condos in Toronto.

The finished building was to have 189 hotel rooms and 612 condominium units. The glass and metal structure would have used the latest environmentally friendly and efficient technology making it one of the greenest condos in Toronto.

#1. Hire a professional like 'ThermaPureHeat' or 'Magical Pest Control' to kill your bed bugs by pumping hot air into your home, at a cost of roughly $1 per square foot this is an expensive method. They pump hot air into your home for several hour, raising the temperature inside to 50 degrees C.

#1. Hire a professional like 'ThermaPureHeat' or 'Magical Pest Control' to kill your bed bugs by pumping hot air into your home, at a cost of roughly $1 per square foot this is an expensive method. They pump hot air into your home for several hour, raising the temperature inside to 50 degrees C. #2. Do It Yourself. You will need an industrial heater, fans and you will want to raise the temperature to 60 degrees C to be extra certain they're all dead. You will also want a thermometer gun and a fire extinguisher to make certain all the places in the home are heated to at least 46 C. The fire extinguisher is in case you have anything combustible that you forgot about.

#2. Do It Yourself. You will need an industrial heater, fans and you will want to raise the temperature to 60 degrees C to be extra certain they're all dead. You will also want a thermometer gun and a fire extinguisher to make certain all the places in the home are heated to at least 46 C. The fire extinguisher is in case you have anything combustible that you forgot about. REMEMBER TO TURN OFF THE FIRE ALARMS! The last thing you need is a false alarm visit from the fire dept. from the heat setting off the fire alarm.

REMEMBER TO TURN OFF THE FIRE ALARMS! The last thing you need is a false alarm visit from the fire dept. from the heat setting off the fire alarm. With that in mind it makes sense to me that people might want to consider buying a house in a region of Toronto which is often overlooked.

With that in mind it makes sense to me that people might want to consider buying a house in a region of Toronto which is often overlooked. I look at the architecture of some of the homes in Leaside and I just drool. They're "perfect", almost idealized, like a Carl Schaefer painting.

I look at the architecture of some of the homes in Leaside and I just drool. They're "perfect", almost idealized, like a Carl Schaefer painting. #1. Conveniently close to both Yonge Street and the Don Valley Parkway. Commute time to downtown is 15-30 minutes.

#1. Conveniently close to both Yonge Street and the Don Valley Parkway. Commute time to downtown is 15-30 minutes. I did manage to find a painting of the octagonal home however, shown here.

I did manage to find a painting of the octagonal home however, shown here. Residential construction in Leaside didn't begin until the 1930s. In 1967 Leaside became part of East York and eventualled was amalgamated with Toronto in 1997. The area is popular with families, since it has such quiet streets, very little crime and a large number of schools / parkland. Many parents consider it to be one of the ideal locations in Toronto to raise kids.

Residential construction in Leaside didn't begin until the 1930s. In 1967 Leaside became part of East York and eventualled was amalgamated with Toronto in 1997. The area is popular with families, since it has such quiet streets, very little crime and a large number of schools / parkland. Many parents consider it to be one of the ideal locations in Toronto to raise kids.